The uses of Activity Based Costing (ABC) can be stated as 1) Understanding of Product, Customer and Channel Profitability 2) Understand the cost of processes and the drivers for those cost 3) Activity Based Planning (ABP). We have seen in the earlier posts a good amount of information on the first two parts of the uses. Today we will talk about the third part that is Activity Based Planning. Activity Based Planning can be divided into two parts a) Activity Based Resource Planning only b) Activity Based Financial Planning.

Activity Based Resource Planning helps to understand the requirement of resources based on the forecast done. In the Activity Based financial Planning, resource as well as costs and revenue are also included to understand the complete profitability for the future period. We will discuss the various steps in this process. The prerequisite for creating the ABP model is that the organization should have a running ABC model.

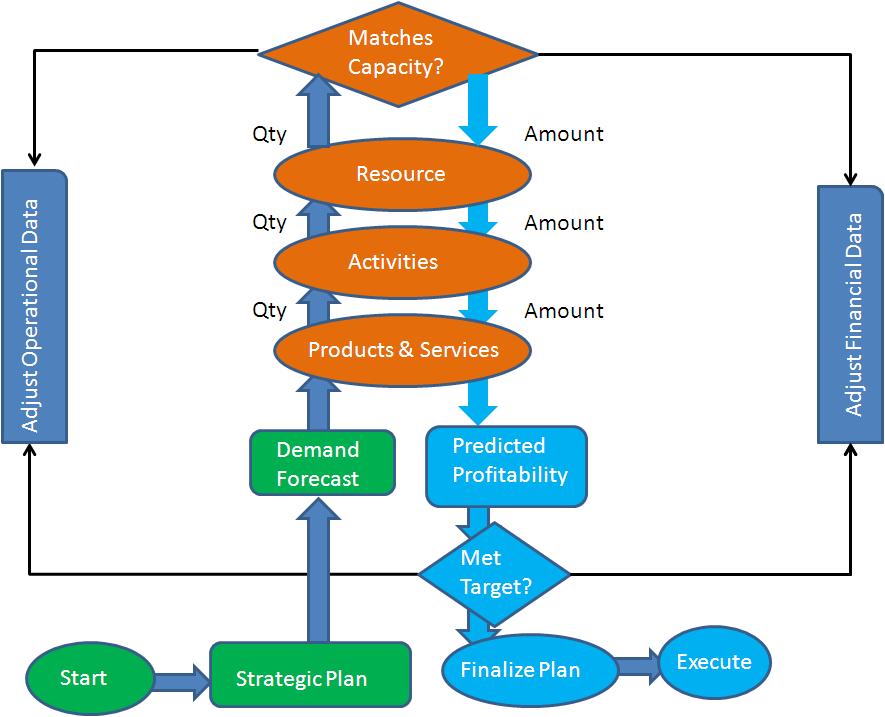

Once the strategic plan has been finalized for the organization (which may state what kind of products to be provided to which customer segments via which channels in the various geographies), it will help the sales function to convert it into the demand. This forecast will be used as the starting point for creating the ABP model. The cost objects as products, customer and channel combination will have the quantities from the sales forecast. These quantities will in turn back calculate the volume of various activities to be performed to fulfill the requirement of various customers. The relation between the products, customer and channels and the activities is used from the ABC model in the organization. In the same manner the resource requirement is calculated from the activity volume. This resource requirement generally talks about the volume of various skills required. For example, 1200 hours of Lathe, 3000 hrs of Sales executive etc. We have to compare this resource requirement with the available resources and see if it fulfills.

If the resource requirement does not match with the availability of the resources then we have perform some operational adjustments. These could be of multiple types.

A) Capacity adjustments – If the required resources are more than the available then we may hire more or we can also transfer skills from other functions where there is excess capacity and the cross-functional transfer is possible. If the available resources are more than the required then one has see if there is scarcity in other functions and if the resources can be transferred there. One has to also see the seasonality of the business, before taking any drastic steps with respect to the excess resources.

B) Consumption rate adjustments – This is nothing but the driver quantities as in ABC. In other simple terms how much time is taken for various activities or how many times an activities is performed to provide a service to a customer. With respect to time taken by activities, internal benchmarking is very useful. You can compare the timing in other plants, branches, location etc. One can also look at the ‘non-value adding’ activities and try to eliminate them. Sometimes few of the customers are making you perform certain activities or their recurrence which is not adding any value to you. In that case a discussion with the customer to make them understand the same is useful. It is also seen that a ‘menu based’ pricing is adopted. One has to understand that even if the customer is ready to pay for the activities, you may face the resource crunch; it is just that you get paid by the customer.

C) Demand adjustments – Once both the above mentioned adjustments are done then we can think of adjusting the demand. This could be increasing or decreasing. Increasing the demand means getting more market share or creating more market segments (by adding customers, regions or products). This has to be seen in conjunction with competition. Reduction of demand because of scarcity of the resources also has to be seen in multiple ways. It may be so that the demand in the market is temporary. If it is a sustaining requirement then investment in the machinery, people etc. can be seen.

As we have seen the adjustments are not always easy as talked here. One has to consider various possibilities and SWAT analysis should be performed. Also it is not so that the adjustment has to be done in this sequence only. Practically it would be various steps with a combination of adjustments.

Once the operational adjustments are competed, we start entering the financial information. The rates for the products or the total revenue, the costs of the resources etc. Once this information is entered we will get the predicted profitability of the organization. This is a combination of product and customer profitability. This value calculated is the result of the strategic initiatives out into action. One may find that the best of the strategy at any point nin time may not be giving you the best of the returns.

If the target for the profitability is not achieved then we can perform the financial adjustments like reducing the resource costs or increasing the price. Both of these could be very difficult to achieve. A practical combination of the same has to be performed.

This is an iterative process of adjustments. The various steps of adjustments or combination of the same can be saves as scenarios. The final accepted model is used as the planned model and the actual results are compared with the same.

In the usual financial budget we perform the comparison of the actual expenses against the plan one, GL account by account. With this comparison the manager is provided with information of favorable or unfavorable variance. With this information the manager can be happy or sad. She can never be wise. He never gets the information how well she has utilized the resources. The comparison of the ABP model with ABC model gives the variance of price, cost as well as resource utilization, activity variance etc. This helps the organization to revisit the strategic initiative to reach to the expected returns from the business.